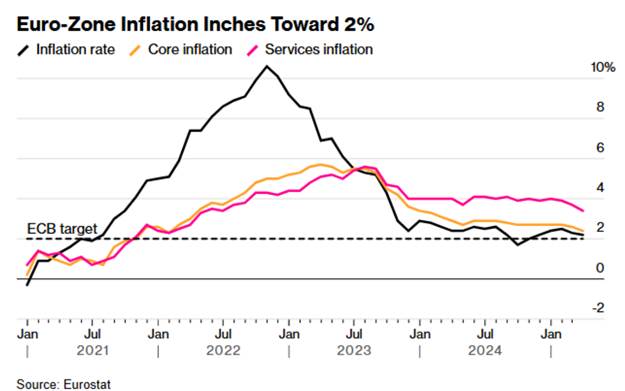

The decline in inflation in the eurozone in March mainly reflects a further easing of services inflation.

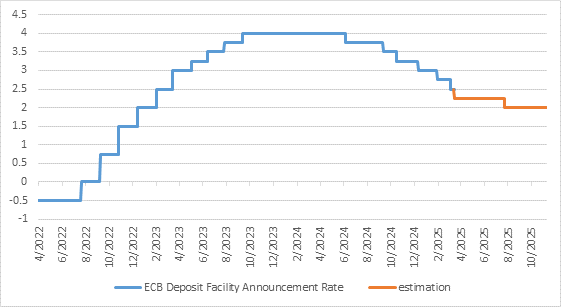

This publication should reassure the ECB, which is expected to lower its rates again in April, even though the future path will depend on the interaction between tariffs and fiscal stimulus on inflation and growth. This decrease is due to the drop in core inflation, itself driven by an encouraging slowdown in services, which fell from 3.7% in February to 3.4%. Energy inflation turned negative in March and offset the rise in food prices.

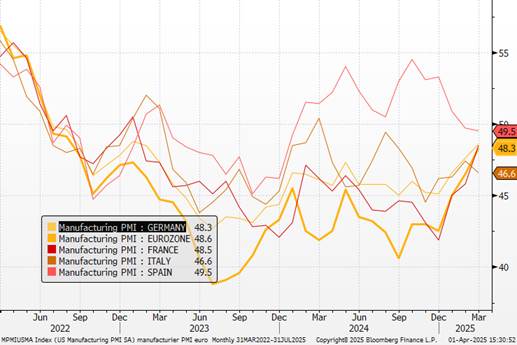

The evolution of headline inflation varies across countries: it declined in Germany and Spain, remained stable in France, and increased in Italy. Nevertheless, core components showed a favorable trend in all major economies of the zone. At the same time, manufacturing PMI indices fell, reflecting a deterioration in order books, particularly for exports, against a backdrop of risks related to tariffs.

Today’s publication bodes well for the continuation of the disinflation process. Services inflation is expected to continue easing, driven by weak demand, favorable price expectations from businesses, and slowing wage growth. We believe these factors will encourage the ECB to cut rates at its meeting this month, although its subsequent decisions will depend on the highly uncertain interaction between tariffs and fiscal stimulus on inflation and growth. Although sentiment in the industrial sector remains subdued, it is gradually closing the gap with that of services. Some signs suggest that the manufacturing recession is nearing its end, particularly in Germany, a country with a strong industrial base.

Manufacturing PMI indicators

In recent months, the labor market has attracted inactive individuals, which has supported the unemployment rate despite rising employment. We believe a sharp deterioration in the labor market is unlikely, and that modest job growth should be enough to support the recovery in consumption, the main driver of growth. This confirms that there is no domestically driven inflationary pressure.

We believe these factors will encourage the ECB to cut rates at its meeting this month, although its subsequent decisions will depend on the highly uncertain interaction between tariffs and fiscal stimulus on inflation and growth. Our target remains at 2% in July. We continue to favor European assets on a relative basis, as visibility is greater in terms of growth and monetary policy.

ECB deposit rate and estimate

{kind=link}