")

US EQUITIES

America, the new swing producer

- The large-scale military offensive by Israel and the United States against Iran, which began on February 28, 2026, risks creating a new prolonged energy crisis. Iranian retaliation has halted oil and LNG trade in the Strait of Hormuz, through which 20% of the global oil and LNG market normally transit, representing approximately 20 million barrels of oil equivalent per day (Mboep/d) and 80 Mt/year of LNG (approximately 2 Mboep/d).

- This conflict is taking place in a context of relative oil abundance. At the end of 2025, the price of Brent crude was around $60, its lowest level since 2022 and compared to an average of $68 in 2018 and 2019. The US Energy Information Administration (EIA) estimated oil overproduction on February 10, 2026, at 2.7 million barrels per day in 2025, rising to 3 million barrels per day in 2026, the highest level since 2016. This led the EIA to estimate the price per barrel at $58 for 2026 and $53 for 2027. In addition, commercial stocks of oil and other liquids in OECD countries reached 2,900 million barrels at the end of February 2026, representing around 30 days of global consumption, to which must be added US strategic reserves of crude oil of 439 million, representing around 20 days of US consumption.

- Between February 27, 2026, and March 6, 2026, the price of Brent crude oil, which already included a risk premium linked to preparations for this offensive, rose from $72 to nearly $90. Over the same period, the price of natural gas in Europe (TTF) rose from $11/mmBtu to $18/mmBtu. On average in 2022, the year of Russia’s invasion of Ukraine, Brent and TTF traded at $99 and $40, creating a strong downward pressure on global economic growth, exacerbated by a major interest rate shock. Since February 27, 2026 long-term rates rose slightly: around 20 bps for the 10-year US and German bonds, the US stock market (S&P 500) is holding up better than the European (Eurostoxx50) and emerging (MSCI Emerging) markets: +1.3%, -6% and -4.8% in EUR.

- In the short term, several reasons lead investors to hope that Iranian interference in the Strait of Hormuz will be limited by: 1- US military supremacy with the help of its Arab allies in the region, and even the use of Ukrainian anti-drone technology; 2- the midterm elections, which should encourage the US to de-escalate tensions; 3- China’s geopolitical pressure on Iran to negotiate; and 4- the ability to divert some of the oil and gas from the Persian Gulf through land pipelines in Saudi Arabia and the United Arab Emirates.

- In the medium and long term, this new crisis should further strengthen the United States role as a regulator of the oil and gas market. According to Yergin, author of The Prize, 1991, a reference book on oil history, the United States relinquished this role in March 1971 to OPEC, when the Texas Railroad Commission authorized the US oil industry to produce at maximum capacity to meet demand. With the shale gas and oil revolution that began in 2008, the United States became a net exporter of crude and refined oil in 2022. In 2026, the United States will be a net exporter of 3 Mboe/day of natural gas and 3.1 Mboe/day of crude and refined oil, according to the EIA.

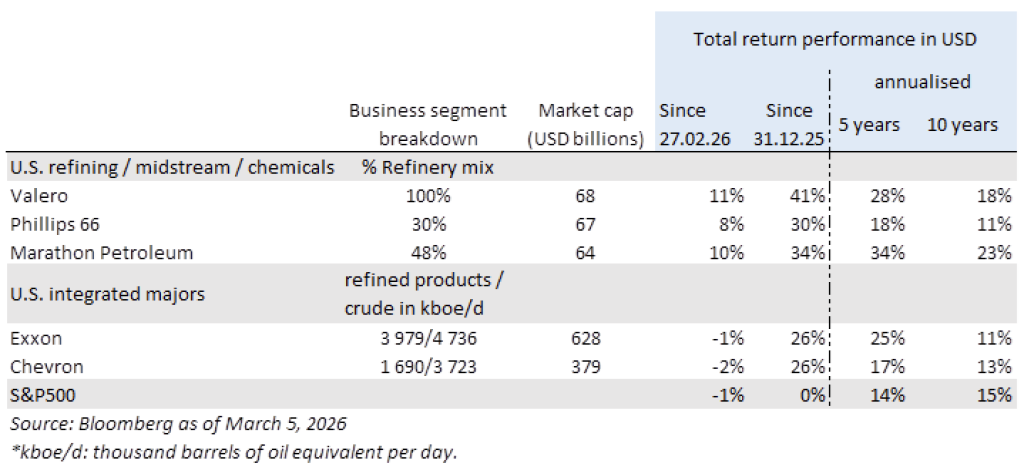

- In our view, this new deal makes US integrated oil majors stocks attractive because their exposure to the Middle East is marginal and their production is growing and concentrated mainly on the American continent. In addition, US refiners are benefiting from very competitive gas prices in the US ($3/mmBtu) essential to refine oil. The 321 crack spread index in Cushing, Texas, a proxy for a US refinery’s gross margin, has skyrocketed since the start of the conflict to $43/barrel on March 5, 2026, compared to an average of $37/barrel in 2022. Their heavy industry complex in the Gulf of Mexico, which is difficult to replicate elsewhere in the world, should continue to be highly profitable.

Written and completed on 06/03/2026

{kind=link}