- COSTCO

- REPSOL

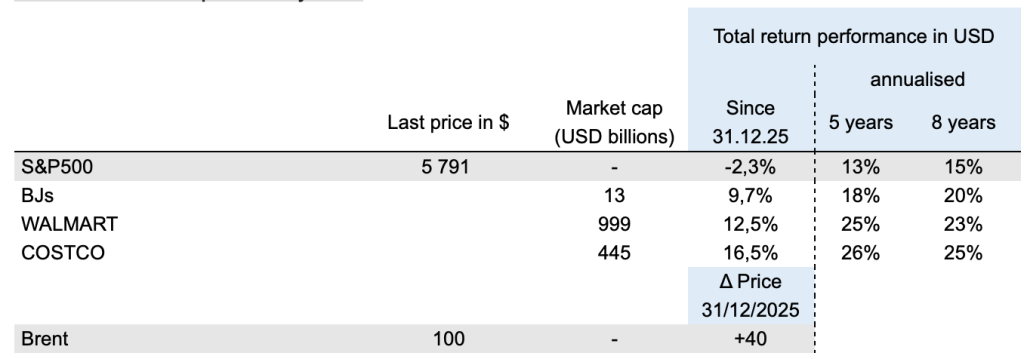

US EQUITIES

Is there going to be a rush to Costco’s gas pumps?

- In response to the surge in oil prices since late February, gas prices at the pump for U.S. consumers have also skyrocketed. The average price of a gallon of gasoline (1 gallon = 3.78 L) across the United States was $4.26 on March 11, 2026, compared to $3.35 at the end of 2025, which was the lowest level since 2021. At its peak in June 2022, the price of gasoline reached $5.50 per gallon. The average American household spent $3,000 per year on gasoline in 2025, the same amount as in 2007. The 2008 recession, followed by the pandemic and the 2022 energy crisis, have led Americans to be more fuel-efficient. Gasoline consumption per household has fallen by about 25% since 2007. Americans are also increasingly filling up at warehouse clubs. The three main warehouse clubs in the United States are Costco, Sam’s Club (owned by Walmart), and BJ’s.

- What sets their business model apart is that, in exchange for an annual membership fee ranging from $50 to $130, customers enjoy a number of benefits.One of the main ones is the highly competitive price at the pump. Unlike Walmart, where gasoline sales are marginal, fuel sales at Costco accounted for 10% of its revenue in 2025 and up to 14% in 2022. Fuel is a strategic loss leader, with a price per gallon that is generally $0.20 cheaper than at a traditional gas station, according to Business Insider. 50% of Costco warehouse visitors also fill up there. The savings generated largely offset the cost of the annual membership. Additionally, Costco offers a limited range of high-quality, frequently replenished everyday items, sold in bulk and largely under its private label Kirkland. Inventory turnover, measured in days of sales, is fast: 28 days at Costco versus 40 days at Walmart. The number of different items (SKUs) is limited to 4,000 per Costco warehouse, compared to approximately 120,000 in a Walmart Supercenter of equivalent size (approximately 15,000 square meters). This notably limits inventory losses and increases its bargaining power with suppliers. Kirkland generates 1/3 of its revenues, $86 billion, which is as much as Procter & Gamble!

- This business model translates into a unique financial model for a retailer. First, its gross margin is very low, 11.1% in 2025, compared to 24% at Walmart. However, revenue from membership cards accounted for 51% of operating income in 2025, Costco operational margin is 3.85%. With only 914 stores at the end of 2025, Costco generated $270 billion in revenue and $10.4 billion in operating income, representing strong profitability per store: $11.4 million in operating income per store on $272 million in revenue per store. Operating profitability per store is therefore 4.2 times higher than that of all Walmart Group stores combined.

- Although founded in 1986, Costco remains a company experiencing strong and steady growth in North America (which accounts for 83% of its revenue) and internationally. In the most recent quarter ending in mid-February, Costco reported a 6.7% increase in same-store sales, with average store traffic up 3.1%. Operating income increased by 12.5%. Over the next 5 to 10 years, Costco plans to expand its store count by 30 stores per year, representing a growth rate of 2-3%, consistent with that of the past five years.

- From an investment perspective, investors view Costco as a high-quality stock that is unlikely to deliver any unpleasant surprises. It is a solid core holding. The valuation is rich (46x forward 12-month earnings). However, we believe this is consistent with expected growth earnings growth in the mid-teens per year, a healthy balance sheet (projected $13 billion in net cash by the end of 2026), and the prospect of accelerated growth in a context where oil prices have risen sharply.

EUROPEAN EQUITIES

Refining margins soar in the wake of the blockade of the Strait of Hormuz

- The war in Iran is clearly evolving into a war over oil: Iran has used drones to attack two oil tankers, claiming that the world should ‘prepare for oil at £200 a barrel’. Normally, one-fifth of the oil traded worldwide (20 Mb/d) passes through the Strait of Hormuz, so its effective closure (with 10% of the world’s tanker fleet blocked in the Persian Gulf) is limiting exports from the region, pushing energy prices higher. Oil-producing exporting countries are busy reorganising their routes, but alternative strategies are limited: Saudi Arabia can redirect up to 7 Mb/d to its terminals on the Red Sea coast, the Emirates can use the pipeline (1.5 Mb/d) from the port of Fujairah (their only major port outside the Persian Gulf), and Iraq can make greater use of its pipeline to Turkey, but exports there are already disrupted. Even if we imagine a scenario in which these alternative routes are operating at full capacity, there is still a shortfall of more than 13 Mb/d.

- The situation is also very critical for liquefied natural gas (LNG), for which Qatar (whose Ras Laffan complex, one of the world’s largest LNG production centers, has been shut down) and the UAE account for one-fifth of global trade. This comes at a time when European gas stocks are low after a harsh winter. The kerosene shortagein Europe (30% of imports came from the Gulf) is severe, with alternative suppliers being costly or too far away geographically, making it the most strained petroleum product in the world.

- Faced with these blockages, the United States has launched a £20 billion reinsurance facility to restore commercial shipping in the strait and, above all, strategic reserves will be mobilised. The International Energy Agency (IEA) has announcedthe largest release of strategic stocks in its history (400 Mb), but this will take time, given that it would take almost 15 days for the release of US strategic reserves to reach the market. This could offset part of the disruption if it is short-lived, but is unlikely to compensate for lost volumes if the situation becomes protracted. We should also bear in mind that this withdrawal from reserves is temporary and will then need to be replenished.

- Which European oil company should be favoured in this context? TotalEnergies, which has underperformed the sector since the start of hostilities, is not the best candidate, as its heavy exposure to upstream production could be disrupted (15% of its production in the Middle East, 34% in MENA). On the other hand, integrated groups such as Norway’s Equinor and Italy’s ENI are highly sensitive to changes in oil and gas prices. Equinor in particular is benefiting from the rebound in gas prices via the TTF index, to which part of its gas sales in Europe are indexed. Nevertheless, since the duration of the rise in energy prices remains a major unknown, as does the outcome of the conflict, it may be wise to position oneself in a group with a more ‘refining’ profile, such as Repsol, as refining margins are likely to remain high for several months, regardless of the outcome of the conflict.

- Indeed, major disruptions in refining complexes in the Middle East (preventive shutdown of Ruwais, one of the world’s largest refineries in the Emirate of Abu Dhabi on the Persian Gulf coast, damage to refineries in Bahrain, etc.) are creating theconditions for a sharp decline in global stocks, a domino effect that seems inevitable given the 1.8 Mb/d of refining capacity currently shut down or operating at reduced capacity. Admittedly, the release of strategic stocks (those in Europe are mainly held in the form of refined products, whereas in the United States they are crude) will ease the pressure for a while (the release of reserves would correspond to 20 days of disrupted flows via Hormuz, but its speed remains limited), but nevertheless, no one will be able to avoid rebuilding distillate stocks. During the invasion of Ukraine, crack spreads (theoretical refining margins) remained high throughout the year, with distillate stocks below historical averages for more than a year, as refineries maximised production to take advantage of high margins.

- Repsol (an integrated oil group with exposure to Europe and the Americas, and one of Europe’s largest distillate producers) currently enjoys a strong strategic position, with one of the highest sensitivities in the sector to changes in refining margins: +/- $1/b generates +/- 3% earnings per share. Thus, strong refining margins in Europe and fuel shortages are boosting the performance of its European refineries and generating robust cash flow in this context of high energy prices. Furthermore, the Spanish group, which plans to reduce its capital intensity upstream, is one of the only players in the sector to have maintained its share buyback program and is expected to see dividend growth of 6-7% per year, while most of its competitors are at +4%.

- We must keep in mind that for any investment in the oil sector at present, the key short-term variables will be the duration of the conflict and therefore the blockage of the Persian Gulf, and the extent of the damage to energy infrastructure. Nevertheless, it seems to us that, whatever the scenario, pressure on refining margins in Europe is likely to remain high.

{kind=link}