- PERNOD RICARD BROWN-FORMAN

US-EUROPEAN EQUITIES

Pernod Ricard – Brown-Forman: Does Unity Bring Strength in a Stagnant Market?

- On March 26, 2026, Pernod Ricard and Brown-Forman confirmed that they were in talks regarding a merger of equals following media leaks. Brown-Forman’s stock surged by more than 20% during the trading session before closing up 9.5%, while Pernod Ricard’s stock fell by nearly 6%. Since Pernod Ricard is likely the initiator, it will have to offer a premium to Brown-Forman shareholders.

- The two leading groups in the spirits market (whiskey, tequila, cognac, vodka, etc.), along with Diageo, are facing a sluggish market. At Pernod, organic growth has been negative since the 2024 fiscal year ending in June (-1% in 2024, -3% in 2025, and -7% in the first half of the 2026 fiscal year). At Brown Forman, growth is sluggish (-1% for fiscal year 2024 ending in April 2024, 1% for fiscal year 2025, and projected at -1% for fiscal year 2026).

- This sluggish growth can be attributed to cyclical factors such as pressure on purchasing power in the West and in emerging markets, as well as weak Chinese consumption, but also to price increases driven by tariffs, particularly in the United States and China. However, the pressure on the spirits market appears to stem more from deeper shifts in consumption patterns, where we are drinking alcohol more occasionally. Pernod’s slogan, “Creator of conviviality,” no longer seems as closely associated with alcohol consumption as it once was. Although their brand portfolios are presented by management as “premium,” Jack Daniel’s (Brown-Forman) and Absolut for example (Pernod Ricard) remain mainstream alcohol brands.

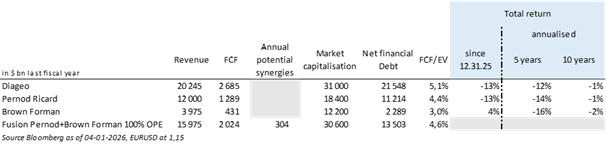

- In theory, a merger between these two groups appears to create shareholder value in the medium term. For Brown Forman, it would accelerate the expansion of its addressable market in emerging countries, which currently account for just over 21% of its revenue, compared to more than 40% for Pernod, particularly in India and China. Furthermore, Brown Forman would benefit from Pernod’s global distribution network. For Pernod, the appeal appears even greater, as it would gain control of a unique whiskey brand, Jack Daniel’s, Brown Forman’s primary asset. Analysts estimate potential annual cost synergies of approximately $300-400 million, a figure yet to be confirmed by management, and despite the restructuring efforts already underway in both groups.

- In practice, bringing together two founding families that are still active and major shareholders in both companies will remain a cultural challenge in managing a merged group.

- From an investment perspective, the spirits sector which has traditionally behaved as a defensive sector during past market corrections remains, in our view, a segment of the market to avoid, given 1) the challenges ahead in the alcohol market, 2) the significant financial debt of these companies, and 3) valuations that remain quite high relative to their growth prospects.

{kind=link}