The SNB has reduced its key interest rate by 50 basis points to 0.5%, with the rate on excess sight deposits lowered to 0%, the Council announced this week, adding that it remains ready to intervene in the foreign exchange market if necessary.

President Martin Schlegel noted that markets were anticipating a terminal rate of 0% by 2025 but avoided commenting on the SNB’s rate trajectory or the certainty of another rate cut. Monetary conditions were “appropriate,” he stated during his first press conference as the Bank’s president, adding that there was room for further policy maneuvering, without directly addressing the possibility of a return to negative interest rates in the future.

SNB Rates and Futures Market

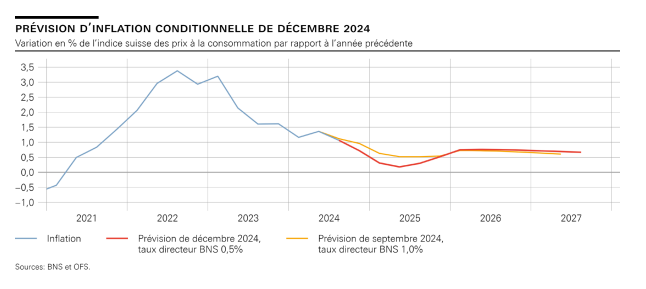

At the September meeting, when rates were cut for the third consecutive time by 25 basis points to 1.0%, headline inflation stood at 1.1% year-on-year and fell to 0.7% in November. SNB President Martin Schlegel, presiding over his first meeting as head, had since stated that “downside risks to Swiss inflation are greater than upside risks.” Policymakers aim to maintain an appropriate policy stance without lagging behind developments. “We want to act early enough to avoid having to overreact later,” he said.

The rate cut came as inflation decreased over the last quarter, with the annual rate falling below the September projection. Without Thursday’s decision, the projection would have been “even lower,” the statement said. However, Martin Schlegel asserted that the SNB does not anticipate inflation entering negative territory on a quarterly basis, although it lowered its 2025 forecast to just 0.3%. While monthly inflation measures may dip into negative territory, the Council would look beyond “temporary deviations” from target levels.

Without committing to a future rate-cutting path, the SNB stated it was prepared to act if necessary to keep inflation aligned with price stability. “The SNB will continue to monitor the situation closely and adjust its monetary policy as needed to ensure that inflation remains within the range consistent with price stability over the medium term,” the statement read. Even with the current low policy rate, there appears to be significant room for further cuts, as Schlegel indicated that negative rates remain a tool at their disposal.

Swiss Rates Over Long Periods

In September, the Council indicated that no changes were planned in the SNB’s foreign exchange market intervention policy, citing the “strong influence of developments abroad on Swiss inflation” and reiterating its commitment to containing the franc’s appreciation.

We anticipate additional deflationary factors next year, such as a reduction in energy prices or a lowering of the benchmark mortgage rate, which is expected to influence rent levels.

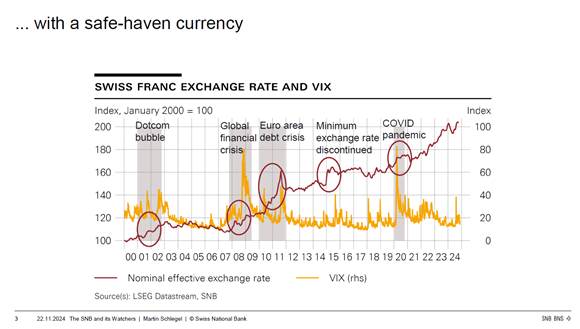

Martin Schlegel delivers a clear signal of determination to combat insufficient inflation on par with that of his predecessor. This marks the first monetary policy announcement of the Schlegel era, as he has served as president of the central bank’s governing board since October 1. It also underscores that the SNB views the trend of Swiss franc appreciation and its consequences as highly risky.

The ECB, without reaching the SNB’s levels of rates, will also need to implement regular rate cuts. Inflationary pressures are likely to continue weakening gradually. At the same time, moderate economic growth is expected to persist, prompting the European Central Bank to maintain its course of action. The Swiss franc’s status as a safe haven is not in question and should remain strong against the euro.

Presentation slides from a BNS meeting in November 2024

We establish a EURCHF range between 0.90 and 0.95 for the next half-year with a target level of 0.94 at 6 months.

EURCHF

{kind=link}