The 3 must-know news stories of the week and What We Think :

- ECB: And That’s Eight

- China: Time for Negotiations

- US: Tariff Effects Begin to Show

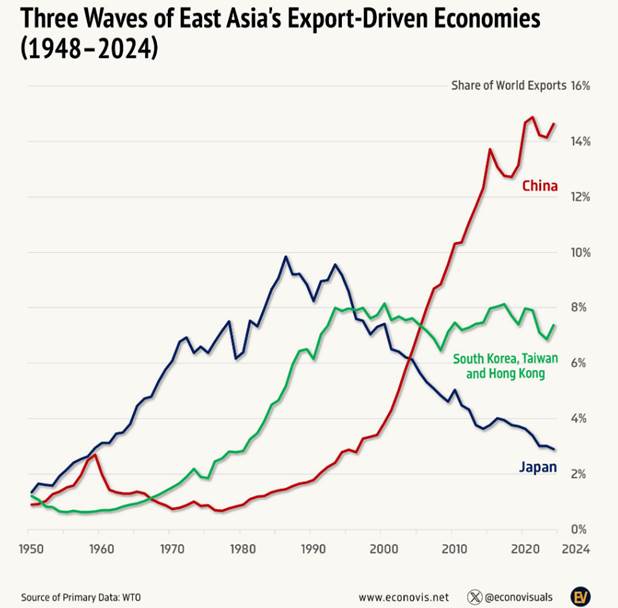

Chart of the week : Historical Economic Perspectives in Asia. What will be China’s trajectory?

ECB: And That’s Eight!

As widely expected, the ECB has cut its three key interest rates by 0.25%, bringing the deposit rate down to 2%. The decision was nearly unanimous, with only one member not supporting the cut. Its president reiterated, as stated in the press release, that monetary policy continues to be guided on a meeting-by-meeting basis, depending on data related to inflation outlook, core inflation, and monetary transmission. The macroeconomic projections confirm the expectation of a return to the inflation target by 2027: now forecasting 2% in 2025 and even 1.6% in 2026, both down 0.3% from the March forecasts due to falling energy price futures and an appreciation of the euro.

Inflation slowed to 1.9% year-on-year in May in the eurozone, falling below the European Central Bank’s target, according to preliminary data published Tuesday by Eurostat. This is well below the levels recorded in April and March (2.2%), and also below economists’ forecasts, who were expecting a 2% inflation rate. On a monthly basis, consumer prices remained stable in May after rising 0.6% in April. This drop in overall inflation below the ECB’s target had only occurred once since June 2021. But it could be more lasting this time if energy prices don’t rebound and if wage growth remains moderate.

Regarding growth, President Lagarde explained that the positive impact of German spending on defense and infrastructure, which will become more visible from next year, should merely offset the negative effect of U.S. tariff measures. This would therefore weigh more on 2026 than on 2025. Risks to growth prospects remain tilted to the downside, as the “exceptional uncertainties” surrounding trade policies are expected to weigh on business investment and exports, especially in the short term.

Notre avis : Even though the 2% policy rate remains broadly neutral, the slowdown in wage growth and the increasing risks of an economic downturn should still support the need for an accommodative policy stance. Notably, the president referred to “the end of a cycle.” The ECB will therefore slow the pace of its rate cuts. However, the European Central Bank could go much further. For now, we expect another 25 basis point cut following the June 5 cut, likely in September, bringing the terminal rate to 1.75%. Another cut remains possible if the economic situation worsens due to the trade war. Both monetary and fiscal policy support continue to create a favorable environment for European sovereign credit. We now expect a pause in July followed by a cut in Q3. Our target has been revised to 1.75%. The ECB will not hesitate to lower rates again if economic conditions deteriorate (which would bring the deposit rate down to 1.50%). We therefore remain positive on eurozone bonds and recommend extending portfolio duration. Unlike U.S. Treasuries, the German Bund remains a benchmark safe-haven asset. The current curve steepness partly shields long-term rates from adverse shocks. We continue to favor Spain, whose fundamentals remain solid. We recommend partial exposure to sovereign credit to benefit from duration within the eurozone. We largely prefer short- and medium-term bonds in the eurozone. Hybrid bonds (which have suffered from rate volatility) remain attractive in a rate-cutting environment. In the high-yield segment, we remain highly selective, though financing conditions are improving significantly. Commercial banks are expected to maintain tight credit standards given the low visibility, and refinancing for the most fragile issuers is likely to become more challenging. Fundamentals for euro IG credit remain solid: euro IG credit spreads are historically tight, near ten-year lows, reflecting strong demand. This is also supported by robust corporate balance sheets. A stable macroeconomic backdrop and the resilience of the European economy should continue to support this asset class. The ECB still holds €315.6 billion in corporate bonds through its purchase programs, representing 27% of the eligible market. Since March 2023, it has been gradually reducing its holdings, but strong investor demand for yield continues to provide support. Liquidity no longer offers sufficient compensation in euros, and we prefer to take positions on longer durations..

China: Time for Negotiations

On Thursday, leaders Donald Trump and his Chinese counterpart Xi Jinping agreed to resume trade negotiations and address the sensitive issue of access to rare earths over the coming months, following a phone call. The relative “thaw” between China and the United States had lasted about three weeks. Tensions between the world’s two superpowers resumed in recent days, less than a month after the May 12 agreement in Geneva.Donald Trump fired the first shot, accusing China at the end of May of having “completely disregarded” the agreement. According to the U.S. president, Beijing continued to block the export of several rare earth elements to the United States despite China’s earlier commitment.

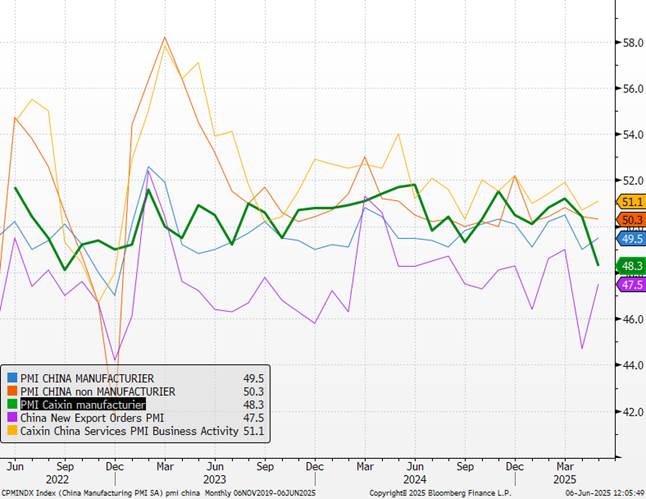

The restrictions imposed by China in May on rare earth exports caused significant disruptions to supply chains, particularly in the automotive sector. The tone escalated further in recent days between the two partners. In retaliation, the Trump administration reportedly blocked the export of American technologies that China needs for its aerospace program. “What China is doing is withholding products that are essential to industrial supply chains in India, in Europe, and that’s not what one expects from a reliable partner,” denounced U.S. Treasury Secretary Scott Bessent. This resumption of talks has revived investors’ hopes that a trade deal may eventually emerge. However, these twists in U.S.-China relations highlight the difficulty and length of the negotiation process, which continues to hinder economic activity due to very limited visibility for businesses. In China, economic activity is already slowing more markedly. The Caixin Manufacturing PMI for May showed a stagnation in activity and revealed the early effects of tariffs affecting the Chinese manufacturing sector. Indeed, the Caixin Manufacturing PMI dropped sharply in May to 48.3, entering contraction territory for the first time in eight months.

It’s worth noting that this index better captures dynamics in the private sector and more accurately reflects SMEs and export-oriented companies, which explains its sharper decline compared to the official PMI. Companies reported a significant drop in new export orders and emphasized that tariffs are strongly dampening demand and new orders, now at their lowest level since September 2022. Employment was not spared either, as Chinese firms are cutting staff through layoffs and not replacing departing workers. However, China’s services sector experienced stronger-than-expected growth in May, according to private purchasing managers’ index data, with robust domestic demand helping to offset the impact of increased U.S. tariffs, which have hurt export orders..

Chart: Leading Indicators in China

Our view : It is difficult to say whether trade tensions will be contained in the second half of the year, but negotiations should have made significant progress by then. Donald Trump’s flip-flops suggest he is more eager for a deal than his “partners.” A substantial share of China’s economic growth in recent years has been driven by strong support for export industries and external trade. In response to the rapid acceleration of Chinese exports, the United States — under Donald Trump — launched a full-fledged trade war. However, Chinese exports are expected to slow significantly in the coming months, especially as many companies have built up inventories ahead of the implementation of tariff barriers. Beijing will therefore need to find new sources of domestic growth. Chinese authorities clearly shifted tone during the “Two Sessions” congress, committing to a more proactive fiscal policy and a moderately accommodative monetary policy. The decline in overall activity, particularly in industry, is largely due to shrinking order books, reflecting weakened domestic demand and limited visibility on economic prospects. Service companies have also cut staff for the second consecutive month to contain rising input costs.

One positive sign is worth highlighting: Chinese household spending increased during the early May holidays, a sign of gradually returning confidence and a willingness to create conditions to boost domestic consumption. We therefore remain broadly constructive on China, though volatility will likely remain heightened due to recurring swings between tension and détente with the United States. The main uncertainty lies in Europe’s stance. Donald Trump’s strategy — including the introduction of a 90-day moratorium — appears aimed at strategically weakening China. It remains to be seen whether Europe will be drawn — likely a key point in the negotiations — into choosing sides and entering a trade war of its own, which would be detrimental to both blocs.

US: Tariff Effects Begin to Show

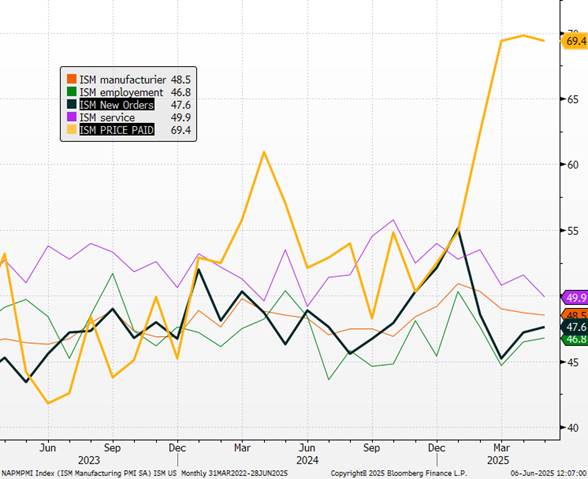

The U.S. economy continues to demonstrate notable resilience, but several indicators are now showing signs of weakness. The ISM Manufacturing Index dropped to 48.5 in May, down from 48.7 in April and well below the consensus forecast of 49.5, marking its lowest level since November (ISM, June 2025). While the “new orders” component remains at a floor rarely seen outside of recessions, the real red flag comes from the sudden rise in the number of firms reducing their imports—evidence that tariff tensions are weighing on supply chains. Tariffs on industrial inputs are now undermining the competitiveness of U.S. small and medium-sized enterprises. Moreover, the “employment” component remains in contraction territory, confirming a downward trend observed for several months. On the services side, the ISM index fell to 49.9 in May from 51.6 in April, far below the expected 52. The dramatic drop in the “new orders” subcomponent to 46.4 is particularly concerning—such a low reading is rare outside of recessionary periods.

While the “employment” component in services is still holding up, the “prices paid” component has risen to its highest level since late 2022, suggesting inflation remains a major concern for businesses. Rising production costs in the services sector are beginning to squeeze margins, which could slow hiring in the coming quarters.Construction spending declined by 0.4% in April—its third consecutive contraction—bringing it down to its lowest level since September 2024 (Department of Commerce, May 2025). The decline is concentrated in residential construction, which is suffering from both high interest rates and rising material costs. Tariffs have driven up the price of imported steel and lumber by nearly 15% year-on-year.

On the labor front, the ADP report showed only 37,000 net new private sector jobs in May—the lowest reading in more than two years. Excluding the leisure sector, job growth was virtually flat. Meanwhile, wage growth for existing employees slowed to 4.5%, its lowest level since June 2021. This reflects a “double bind”: slower wage growth while inflation remains persistent. Lastly, new car sales fell by 8% in May, a direct consequence of tariffs imposed on imported vehicles since the end of April 2025 (Bureau of Economic Analysis). This contraction in the auto market reflects not only the impact of protectionist measures, but also consumer sensitivity to rising interest rates, which are eroding purchasing power: auto loan rates have risen from 5.2% in January to 6.3% in May.

Chart: Leading Indicators in US

Our View: From an economic standpoint, the United States is expected to avoid a recession in 2025, with growth remaining resilient at 1.4%. However, risks are increasing toward the end of the year. Recent trade negotiations suggest that the U.S. administration is seeking to secure deals. The postponement of the most extreme tariffs between the U.S. and China also allows for the deployment of other buffers: U.S. tax cuts and deregulation efforts. Faced with a deteriorating bond market and growing opposition from business leaders and Republican lawmakers, the U.S. president already announced a 90-day truce on reciprocal tariffs, just a week after declaring “Liberation Day.” Still, the trade tensions are far from resolved: new specific tariffs could be introduced by the president at any time. This period is fertile ground for policy reversals. Trump must reassure a Congress hungry for fresh revenues and uphold his promises to reduce the deficit before July 4.

In the House of Representatives, the federal budget bill was passed by a razor-thin margin (215 votes to 214), forcing the president to exert influence to secure support. The bill—over a thousand pages long—includes the extension of the major 2017 tax cuts. Modestly named the One Big Beautiful Bill Act, it aims to roll out a series of fiscal and budgetary measures central to the new president’s political agenda. Many voices warn that it could significantly widen the U.S. fiscal imbalance. Though it may still be slightly amended by the Senate, the Congressional Budget Office (CBO) estimates that it would add $3.1 trillion to public debt over the next decade ($200–$300 billion per year, or +1 percentage point of nominal GDP in 2025). The CBO does not factor in additional tariff revenues, which remain the cornerstone of the bill’s financing. Trump is under pressure and must maintain credibility with Congress.

Across the Atlantic, the EU—despite its strong negotiating capacity as shown during Brexit or the sovereign debt crisis—typically moves slowly and is struggling to deliver a swift response. The grace period before sanctions take effect is designed to accelerate talks in favor of the Americans. Currently, European VAT appears to be a key point of contention: U.S. exporters face a competitive disadvantage versus European companies, which do not apply VAT to goods bound for export. So far, negotiations have been fraught, with no clear common ground. Any unilateral U.S. demands that would infringe upon the EU’s autonomy in regulatory or tax matters will likely remain red lines. As with China, Trump’s backtracking appears more defensive than strategic—meant to avoid an extreme scenario. But what will happen on July 9, 2025?

Time is running out for the president, who is eager to implement his agenda quickly to demonstrate the benefits of his policy before the 2026 midterm elections. The Fed’s stated intention to avoid intervention in response to economic destabilization and persistent inflation risk also raises questions. Economic data remain solid, even though soft data are deteriorating. There is no urgency: in this uncertain fiscal and trade environment, we believe the Fed will wait at least until September—once it has greater clarity—before resuming monetary easing. Q1 results remain satisfactory; however, positive surprises mask disappointing revenue figures.

Surveys showing that business leaders intend to pass tariff-related cost increases on to consumers are hardly reassuring. The standoff between the U.S. president and the Fed chair is only just beginning. While current activity indicators do not yet signal a downturn, inflationary pressures are likely to persist. We therefore maintain a relatively cautious strategy on equities, with a negative view on the U.S. market. We are awaiting a clear de-escalation in trade tensions and a shift in Fed policy, beginning with a rate cut that we expect to continue. July should bring answers, as it marks the end of the tariff moratorium and a scheduled FOMC meeting. We recommend selective stock-picking focused on high-quality names.

{kind=link}