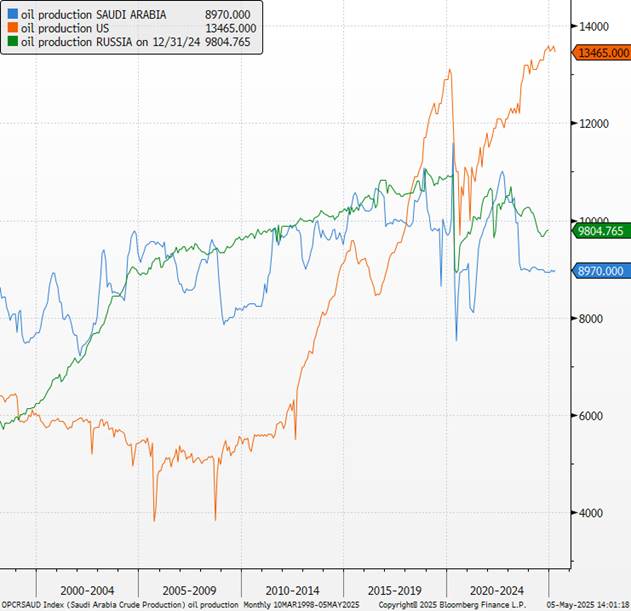

The OPEC+ member countries announced on Saturday, May 3, an additional increase in their oil production, amounting to 0.4 million barrels per day (Mb/d) starting next June. This increase will be distributed among eight members of the cartel, notably Saudi Arabia and Russia, who had until now borne a large share of the additional efforts.

Even though the market had already anticipated these increases, OPEC also mentioned the possibility of extending this monthly pace of increase until November. This decision comes in a context of historically low global inventories and reflects a clear strategic intention: to exert direct pressure on American shale oil producers in the battle for market share. Indeed, OPEC+ members are witnessing a structural loss of their market share in favor of non-cartel producers. The additional supply aims to reach a total increase of 2.2 million barrels per day by November 2025.

However, internal discipline within OPEC+ remains a major challenge. Three countries in particular— Iraq, Kazakhstan, and the United Arab Emirates—are producing about 1.2 Mb/d more than the quotas set. Kazakhstan has even explicitly stated in recent weeks that it is prioritizing its own economic interests over the commitments made to the cartel, thus underscoring its limited interest in strictly adhering to the quotas.

Oil Production

This decision to increase production also reflects the relatively low levels of global inventories, exacerbated by supply difficulties in Venezuela and the stagnation of American shale oil. It also aims to improve compliance by certain countries, notably Iraq and Kazakhstan.

For Saudi Arabia, this measure also represents a gesture toward the Trump administration, which has been actively advocating for lower oil prices, both for domestic political reasons (to reduce gasoline costs and boost Americans’ purchasing power) and foreign policy reasons (to increase economic pressure on Russia). Saudi Arabia, which is struggling to balance its national budget due to low oil prices, has adopted this strategy that is expected to lead to lower prices for the rest of the year. In any case, OPEC+’s decision to inject more oil into a declining market marks a significant shift in approach.

In terms of market analysis, our outlook on oil remains negative. The risks surrounding OPEC+’s supply outlook appear skewed to the upside, which increases the downward pressure on our price forecasts. Despite still-tight near-term fundamentals, the large excess capacity and the heightened threat of a global recession create a context favorable to sustained downward pressure on oil prices. In the short term, stabilization is likely, but we maintain our forecast of persistent pressure on Brent and WTI prices in the coming months, with a supply-demand imbalance more pronounced than initially anticipated.

WTI and Brent prices

On the macroeconomic front, this decision should help moderate inflation, particularly in Europe, thereby offering the European Central Bank greater flexibility to lower interest rates without the fear of imported inflation. (See: https://news.banquerichelieu.com/en/2025/04/25/market-flash-eurozone-ecb-in-support/)

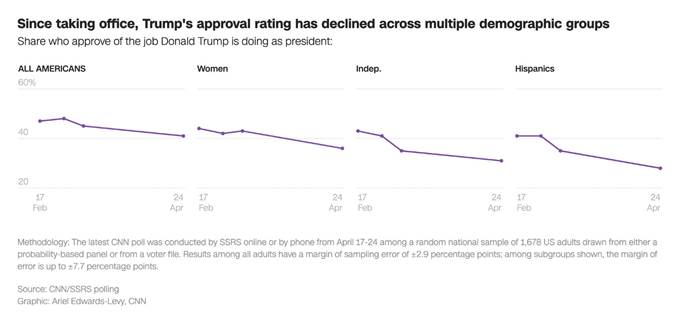

Politically, this development provides indirect support to Donald Trump, who is facing declining poll numbers due to growing voter concerns about purchasing power, particularly affected by fuel prices.

Finally, at the microeconomic level, the current decline in oil prices poses a direct threat to the profitability of American producers, particularly those specialized in shale oil. We maintain our negative outlook, with a WTI price target of USD 60 (with short-term downside risk), a critical threshold below which the profitability of many American producers would be compromised.

{kind=link}