Donald Trump announced last night massive tariff increases targeting Europe and Asia, with a 10% tax threshold for all countries exporting to the United States. The general 10% tax will come into effect on April 5, and the increased tariffs on April 9. Specifically, goods from the EU will face a 20% tax. These rates have been set at 24% for Japan, 26% for India, and 46% for Vietnam. Chinese imports will be subject to an additional 34% tariff (on top of the 20% already imposed since January), and Taiwan to 32%. On average, tariffs are rising to a level well above consensus expectations.

While one might be led to believe that compromises could be found on both sides in order to return to lower tariff rates, Donald Trump’s rhetoric does not support this view. He described these increases as “lenient” measures, claiming they amount to only half of what other countries would apply (according to the U.S. administration) to American products. During a ceremony held at the White House, before signing a presidential decree formalizing these measures, the President of the United States presented a chart listing countries or economic entities, indicating on the one hand the rates applied to American imports according to the Trump administration’s calculations, and on the other hand the future reciprocal tariffs to be imposed by the United States.

This sharp increase poses a major risk to U.S. growth since, assuming full pass-through to the final consumer, the additional cost would generate approximately 3% extra inflation. Real wages (that is, adjusted for inflation) could then turn negative, leading to a contraction in consumption and potentially a recession in the United States.

The stagflation scenario, which we regularly discuss, is thus taking shape, and the markets will continue to adapt to it. Deepseek, the trade escalation, and Trump’s rhetoric are all factors likely to weaken the entire spectrum of American economic actors. (https://news.banquerichelieu.com/2025/03/31/point-macro-economique-avril-2025/)

Economic indicators are deteriorating (moderately so far), and inflation is expected to remain high. Consumers will see their purchasing power decline. The most affluent category will be the hardest hit: those whose wealth has significantly increased since the Covid period, thanks to real estate and financial markets.

The Fed finds itself in a contradictory situation: inflation remains persistent even as the labor market deteriorates, which prompts it to keep its key interest rates at a high level. Corporate profit margins will erode. Tech companies will face retaliatory measures from other countries. Refinancing operations will become more complex, particularly for the most vulnerable players.

“Trump 1.0” relied on stock market indices as real-time indicators of confidence in his tax program. “Trump 2.0” has shifted perspective: he now prioritizes the 10-year Treasury yield as the barometer of his administration. A recession does not scare him. Short-term movements in financial markets are of little importance. The implementation of his political agenda (supported by J.D. Vance, see:https://news.banquerichelieu.com/2025/03/31/ledito-avril-2025/) is the immediate objective. Donald Trump’s term began with potential major geopolitical victories (Ukraine, Gaza), but the second phase is entirely different in terms of the global economy. Domestic American concerns are now at the heart of his current actions.

The president faces a fairly narrow window of opportunity and is under pressure:

· His slim majority in the House of Representatives forces him to make massive spending cuts and generate significant additional revenue.

· The midterm elections will take place in November 2026, and he must show, as early as next year, positive effects of his policy on purchasing power and household confidence, even if it means triggering severe short-term deterioration.

We were already negative on U.S. assets, whether equities or lower-rated credit bonds, and we are reinforcing our view by further downgrading these asset classes. At this stage, there is an increased risk of renewed inflationary pressures, which will hold back the Fed in its desire to ease monetary policy and, in the coming weeks, will fuel fears of potential stagflation.

When to return to U.S. markets?

For now, there is clearly no “Trump put.” We are waiting for a “Powell put,” which won’t be coming anytime soon. Current data still show a degree of resilience in the economy, albeit modest. The Fed is stuck. Paradoxically, a recession would be good news, as it would force the central bank to act. In a second phase, procyclical measures (deregulation, tax cuts) will be implemented. But Donald Trump is starting off with a heavy hand. In the meantime, markets will waver and adjust their valuations downward. As we wrote… patience is key. (https://news.banquerichelieu.com/2025/03/12/flash-marches-quand-revenir-sur-le-marche-americain/)

In terms of assets

Equities

We are entering a phase of significant turbulence, with a new high level of tariffs in the United States. For now, we reiterate our cautious stance toward equity assets, which will remain vulnerable until there is more clarity regarding trade tensions. We are particularly negative in the short term on U.S. equities, which will experience massive outflows (reflecting the scale of inflows in recent years). We are downgrading our recommendation regarding Japan: the specific tariff increase on Japan (+24%) ends hopes for a rate hike by the Bank of Japan (BoJ), as Japanese growth—which is highly dependent on foreign trade, especially with the United States—is now under threat. As for emerging markets, sentiment remains broadly negative. The tariff differential is significant, and most of these countries lack the capacity to negotiate or retaliate, unlike other major powers. Relatively speaking, we favor countries and regions that are capable of negotiating, implementing retaliatory measures if necessary, and supporting their domestic economies through stimulus plans. Europe and China appear to be the main candidates. Defensive sectors should be prioritized. Major tech companies are likely to remain impacted, weakening global indices.

Main stock indices since Donald Trump’s election

Interest rates

In the United States, sovereign bonds are facing contradictory forces: on one hand, inflationary pressures; on the other, a potential recession scenario. We forecast an average 10-year yield around 4%, with a wide range (3.5–4.5%) due to prevailing uncertainties. In general, we remain cautious on lower-quality bonds (high yield, emerging markets) and are particularly negative on U.S. high yield. We strongly favor high-quality bonds in the eurozone. Inflation there is less sensitive than in the U.S., the European Central Bank is expected to maintain its accommodative policy (notably due to a sharp slowdown in wages within the global context), and both European and German stimulus plans will gradually be rolled out..

US & Europe HY Spreads

Currencies

Our stated target was 1.10. At the beginning of the year, we had strong confidence in the dollar, given the outlook for reform. Since then, the situation has changed and perception has reversed (Deepseek, higher-than-expected tariffs, European plan). Trump’s policy is based on accelerated reindustrialization driven by the trade war and, secondly, by a weakening of the dollar. The prospect of a new Fed chair next year, supported by Trump, is expected to further reinforce this trend. More broadly, the current environment is gradually eroding confidence in the U.S. dollar as the reference currency for the global system (reserve currency, trade currency, safe haven). Our new target is now between 1.15 and 1.20 over a one-year horizon.

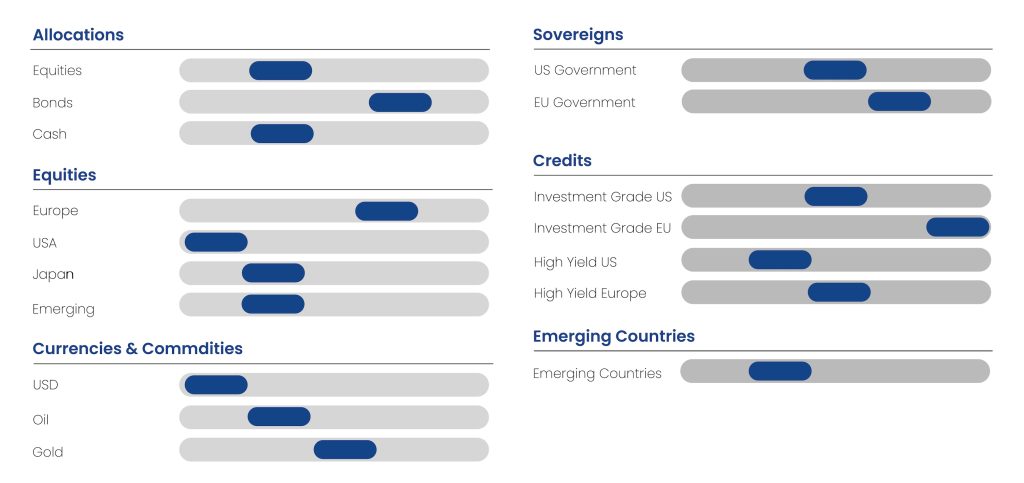

General tactical asset allocation table

{kind=link}