The 3 must-know news stories of the week and What We Think :

- TRUMP hits hard, very hard

- China: the dangerous escalation

- Europe: VAT in the crosshairs

- Chart of the week: stock indices since the beginning of the year

TRUMP hits hard, very hard

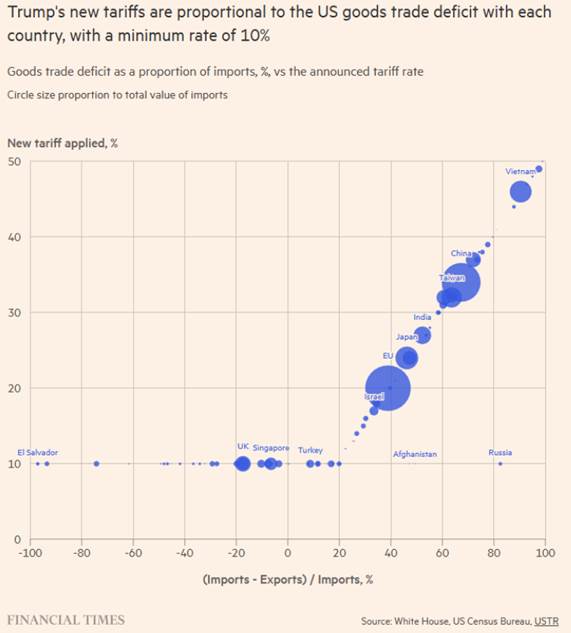

Donald Trump announced this Wednesday massive tariff hikes targeting Europe and Asia, with a 10% tax threshold for all countries exporting to the United States. The general 10% tax will come into effect on April 5, and the increased tariffs on April 9. Specifically, goods from the EU will be subject to a 20% tax. The rates have been set at 24% for Japan, 26% for India, and 46% for Vietnam. Chinese imports will face an additional 34% in tariffs, and Taiwan 32%. While one might think that compromises could be reached on both sides to return to lower tariff levels, Donald Trump’s rhetoric does not point in that direction. He presented these hikes as “lenient” measures, claiming they are only half of what other countries supposedly impose on American goods, according to the U.S. administration. This sharp increase poses a major risk, potentially triggering a contraction in consumption and even a recession in the United States. The formula used to calculate the tariffs, published by the U.S. Trade Representative, took the U.S. trade deficit in goods with each country as a presumed indicator of unfair practices, then divided it by the value of goods imported into the U.S. from that country. However, trade balances are influenced by a multitude of economic factors, not simply by the level of tariffs.

Our view: The stagflation scenario, which we have been discussing regularly, is now taking shape, and markets will continue to adapt to it. The trade escalation and the reactions of the affected countries will lead to significant volatility. We were already negative on U.S. assets—both equities and lower-rated credit bonds—and we are reinforcing our view by further downgrading these asset classes. At this point, there is an increased risk of renewed inflationary pressures, which will hinder the Fed in its efforts to ease monetary policy and, in the coming weeks, fuel fears of potential stagflation. We are waiting for a “Powell put,” which is not likely to come anytime soon. Current data still show some, albeit modest, resilience in the economy. The Fed is stuck. Once the dust settles, procyclical measures (deregulation, tax cuts) will be introduced. But Donald Trump is starting by hitting hard. In the meantime, markets will doubt and adjust their valuations downward. We are entering a phase of major turbulence. For now, we reiterate our cautious stance on equities, which will remain vulnerable as long as there is no greater clarity on trade tensions. We are particularly negative in the short term on U.S. equities, which will face massive outflows (reflecting the scale of inflows in recent years). We are downgrading our recommendation on Japan: specific tariff hikes on Japan (+24%). Relatively speaking, we therefore favor countries and regions capable of negotiating, implementing retaliatory measures if necessary, and supporting their domestic economies through stimulus plans. Large tech stocks are likely to remain affected, weakening global indices.

China: a dangerous escalation

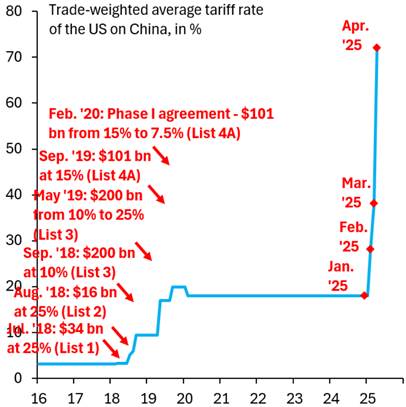

China has retaliated against the new U.S. tariffs with a series of measures, including levies on all American imports and export controls. Beijing will impose a 34% tariff on all imports from the United States starting April 10, matching the level of Trump’s so-called reciprocal tariffs. Chinese authorities also announced immediate restrictions on the export of seven types of rare earth elements (samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium), thereby fulfilling their promise to respond after President Donald Trump imposed tariffs, further intensifying a trade war. They will also launch an anti-dumping investigation into medical CT scanner X-ray tubes from the U.S. and India, and suspend imports of poultry products from two American companies. Additionally, they are adding eleven U.S. defense companies to a list of unreliable entities and imposing export controls on sixteen American firms. China’s measures come in response to Trump’s announcement of reciprocal tariffs on global trading partners. The latest U.S. tariffs will raise levies on nearly all Chinese goods to at least 54%, a move that could cripple Chinese exports to the United States. Tensions between Washington and Beijing have worsened since Trump’s return to the White House in January. Notably, the U.S. president has yet to speak to his Chinese counterpart more than two months after taking office. They also remain at an impasse over China’s alleged role in the influx of fentanyl into the United States, which Trump cited as a reason for the two previous rounds of tariffs.

Our view: Since the Deepseek affair, relations between China and the United States have deteriorated. Chinese innovation is prompting major U.S. companies to question the sustainability of a model that had long been praised. Unlike in 2017, China no longer seems to fear Donald Trump. The escalation of the trade war with the United States poses a significant risk to global growth. In response to these turbulences, China will seek to strengthen its ties with Europe. On the occasion of the 50th anniversary of diplomatic relations with the European Union, Beijing has revived the Comprehensive Agreement on Investment, which had been frozen since 2021. Chinese official Wang spoke of “new goodwill gestures” to relaunch exchanges, including full visa liberalization for OECD countries and improved access for foreign companies to Chinese markets. Economically and geopolitically, China is no longer the same as in 2017 in its dealings with Donald Trump: it now has negotiation capabilities it lacked at the time and has caught up technologically, becoming a serious competitor to U.S. leadership. Trade flows have been redirected toward other countries, shifting the risk onto them for their exports, and less so on China. In his recent statements, Donald Trump suggested that the measures in place were “lenient”… He will not hesitate to strike back. China is reluctant to devalue its currency so as not to hurt domestic consumption, but a full-blown escalation is a dangerous trap. We remain negative on all risky assets.

Europe: VAT in the crosshairs

” “We are now going to make the European Union pay. They are very, very tough traders. You think the European Union is friendly, but they’re ripping us off. It’s so sad to see. It’s pathetic,” said the U.S. president yesterday to justify the measure.

President Donald Trump’s administration supports reciprocal tariffs between the United States and Europe. In Europe’s case, there is a clear argument for action. Tariff rates between the U.S. and Europe are relatively low, but U.S. officials have determined that Europe’s competitive edge mainly stems from non-tariff barriers, notably how it applies the value-added tax (VAT). A recent White House memo cited VAT as one of the unfair, discriminatory, or extraterritorial taxes imposed by trade partners that the U.S. seeks to challenge. For example, European companies such as car manufacturers do not pay VAT on goods intended for export. For the European Commission, this is a fundamental principle. The problem for U.S. companies exporting to Europe is that it places them at a competitive disadvantage. A German carmaker can sell in the high-tax European market or export to the lower-tax U.S. market, benefiting from a VAT rebate. By contrast, a U.S. carmaker must compete with local manufacturers in Europe without enjoying export subsidies. This issue dates back to the 1960s (when VAT was adopted in Europe). In 1971, then-Under Secretary of the Treasury Paul Volcker helped introduce a new fiscal vehicle that reduced the tax burden on U.S. exports. The DISC (Domestic International Sales Corporation) status was gradually phased out starting in 1984, after the U.S. introduced a new mechanism called FSC (Foreign Sales Corporation) in response to international pressure, particularly within the GATT (General Agreement on Tariffs and Trade) framework. After the WTO declared the FSC system illegal, it was abolished in 2004. “Europe is ready to respond,” said European Commission President Ursula von der Leyen, adding: “We will always defend our interests and our values. We are ready to move from confrontation to negotiation.” The European Commission, which is responsible for trade, has been preparing its response for weeks, but European leaders are still counting on a deal with Washington to avoid the worst, believing there is room to negotiate, as the White House’s game is dangerous for growth on both sides of the Atlantic.

Statement by Ursula von der Leyen

Our view: The European response is planned in various forms. However, it may go beyond tariffs. If the response follows a strict tit-for-tat logic, it could also negatively affect Europe, leading to higher inflation and lower growth. A more strategic approach would be a targeted response against select companies. Annual trade between the United States and the European Union amounts to around €1.5 trillion, with a €150 billion surplus in favor of Europe. However, American digital giants generate 25% of their revenues in Europe each year. As a result, U.S. tech stocks would be directly impacted. This could take the form of regulatory retaliation or an acceleration of support plans aimed at boosting domestic investment. The main economic risk remains the creation of inflation. We believe it should remain contained in Europe. In the equity market, relatively speaking, we therefore favor countries and regions capable of negotiating, implementing retaliatory measures if necessary, and supporting their domestic economies through stimulus plans. Europe, if it remains united, appears to us as a strong candidate. Defensive sectors should be prioritized. Large American tech companies are likely to remain impacted, further weakening global indices.

{kind=link}